New analysis shows the COVID-era Early Release of Super Scheme could hit Australian taxpayers with an up to $85 billion bill (in today’s dollars) - mostly due to the higher pension costs of those who withdrew their savings needing to rely more heavily on government support in retirement.

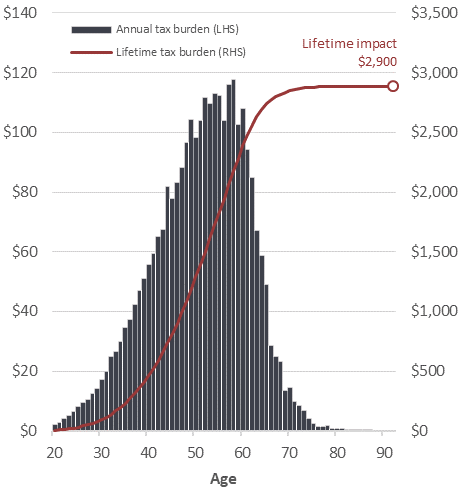

All of today’s 20-year-olds are projected to pay about $3,000 more tax to cover the higher pension bill caused by the scheme, which saw 3 million Australians withdraw $38 billion from super before retirement.

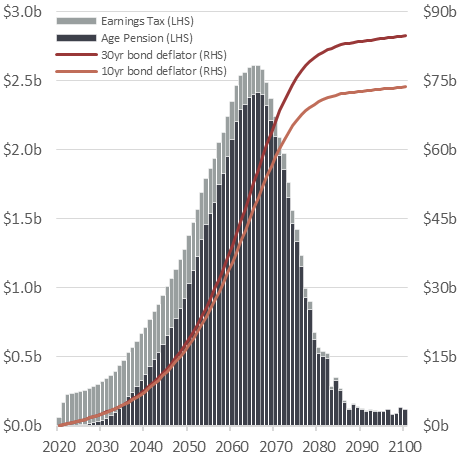

The new Super Members Council modelling shows the early release scheme’s costs in higher pensions and lower super tax receipts are expected to peak at $2.5 billion a year by the mid-2060s.

SMC cameo analysis shows that a 30-year-old who withdrew $20,000 from super could be left with about $93,600 less at retirement – leaving them dramatically worse off in their lifetimes.

Compound earnings makes up three quarters of a super balance at retirement making it difficult to recoup those losses. People who accessed their super before retirement are projected to need to draw more heavily on an age pension, which hikes the pension bill for future taxpayers.

Super Members Council CEO Misha Schubert said the financial toll of the early release scheme would cost both the people urged to withdraw their super and all Australian taxpayers for decades to come.

“In the early stages of the COVID pandemic, before Government assistance kicked in with JobKeeper, many Australians were encouraged to sacrifice their retirement savings to support themselves. Tragically, that will now leave many people significantly poorer in retirement.”

“Those withdrawals will also cost the next generation of taxpayers in a case of fiscal long-COVID.”

“These are the devastating consequences of schemes that break super’s preservation rules. People are left with far less money at retirement, and the next generation – our children and grandchildren – will have to pay higher taxes to pick up the bill for higher pension costs.”

The Super Members Council analysis of the Early Release of Super scheme found:

- The early release scheme will cost taxpayers between $75 billion and $85 billion by the end of the century in higher pension expenditure and lower superannuation tax receipts – which is around double the amount withdrawn from super during the scheme

- All Australians will pay more to meet the cost of the scheme – either through higher taxes or fewer government services – it is estimated today’s 20-year-olds will pay $3,000 more tax over their lifetimes

- A person aged 30 (the median age of withdrawers) who withdrew the full $20,000 (as around half of people did), is expected to retire with around $93,600 less in superannuation

- Approximately 725,000 Australians effectively wiped out their superannuation accounts - of these, 45 per cent were aged 25 and under, and 70 per cent were aged 30 and under

The Super Members Council analysed the Early Release of Super Scheme’s impact to inform its submission on the Australian Government’s proposal to enshrine super’s purpose in law. The Objective of Super Legislation is before Parliament this week.

SMC strongly supports the passage of the legislation – which reflects the views of everyday Australians.

“Ask Australians what super is for, and they’ll tell you it’s their money for retirement. The ‘objective of super’ legislation will reflect that clear and compelling purpose in ironclad law. It will be a guiding light for all future super policy development.”

“We strongly support the legislation. It will ensure super stays strong and secure – and continues to deliver a financially secure retirement for millions of everyday Australians.”

The analysis shows the Australian Government is right to safeguard super’s preservation policy – the principle that the clear purpose of super is to deliver retirement income – in legislation.

Other proposals that promote the early withdrawal of super would similarly leave people worse off in retirement, push up costs for taxpayers, and risk weakening super returns for all Australians.

Recently, these proposals have included using super for:

- to quarantine for health and aged care costs

- a house deposit

- to meet every-day cost of living expenses

- purchasing household electric appliances

- to pay off HECS and other debts.

The Super Members Council supports the Australian Government’s proposal to enshrine the purpose of super in law. The legislation says super’s role is to preserve savings to provide income in retirement in an equitable and sustainable way.

Media contact: James Dowling 0429 437 851, jdowling@smcaustralia.com

Figure 1: Long-term federal budget costs of the COVID Early Release of Super Scheme

|

Aggregate cost |

Tax burden for individual aged 20 now |

|

|

|

Source: SMC analysis using the Superannuation Pensions and other Retirement OUTcomes (SROUT) model.

Key Facts:

— The Covid-era early release of super scheme will cost taxpayers between $75 billion and $85 billion by the end of the century in higher pension expenditure and lower superannuation tax receipts – which is around double the amount withdrawn from super during the pandemic

— All Australians will pay more to meet the cost of the scheme – either through higher taxes or fewer government services – it is estimated today’s 20-year-olds will pay $3,000 more tax over their lifetimes

— A person aged 30 (the median age of withdrawers) who withdrew the full $20,000 (as around half of people did), is expected to retire with around $93,600 less in superannuation

— Approximately 725,000 Australians effectively wiped out their superannuation accounts - of these, 45 per cent were aged 25 and under, and 70 per cent were aged 30 and under

About us:

We are the collective voice for more than 10 million Australians who have over $1.45 trillion in retirement savings managed by profit-to-member superannuation funds. Our purpose is to protect and advance their interests throughout their lives, advocating on their behalf to ensure superannuation policy is stable, effective, and equitable.

Contact details:

James Dowling: 0429 437 851, jdowling@smcaustralia.com