Australia’s dairy sector saw some small increases in farmgate milk prices in recent months, but a softer global commodity market will likely limit further ‘upside’ for the rest of the season, Rabobank says in a recently-released report.

However, Australian dairy farmers will avoid lower returns in the short term with guaranteed prices locked in till the end of the current season, which finishes on June 30 next year, the specialist agribusiness bank says.

In its Q4 2025 Global Dairy Quarterly, the bank’s RaboResearch division said with Australian milk production down in the season to date, there had been small increases (of AUD 0.10/kgMS) announced in October by some major dairy companies in southern Australia, taking weighted average prices to AUD 9.05/kgMS or higher.

But a softer global dairy commodity market – which weakened through Q3 2025 before falling sharply into Q4 – will likely limit Australian milk prices to close out the current season.

RaboResearch senior dairy analyst Michael Harvey said the global dairy market is expected to face a period of weaker commodity prices following “stunning” global milk production growth across the second half of 2025.

Mr Harvey said global milk production growth is estimated to have peaked in Q3 2025, with Q4 growth likely to be not far behind.

Surging global production

“The EU and UK posted their strongest growth since 2017 for the month of October, while surging October milk flows saw the US post its fifth consecutive month where growth rates have been over three per cent,” he said.

“Not to be outdone, New Zealand farmers have been setting new milk solid records each month from May to September 2025, with the peak month of October the third highest output on record.

“And South America is also shaping up to deliver a significant annual volume increase.”

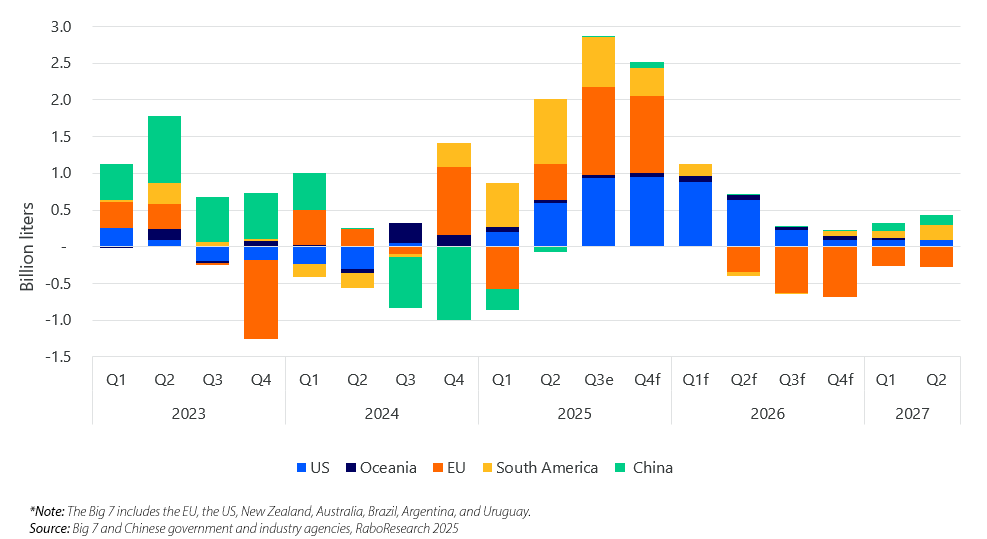

Mr Harvey said combined output from the ‘Big-7’ global dairy producers (the EU, the US, New Zealand, Australia, Brazil, Argentina and Uruguay) is forecast to finish 2025 up 2.2 per cent year-on-year.

And this “wave of milk” had softened dairy markets through Q3 2025, with sharp price falls recorded in Q4, he said.

Milk production growth, Big-7 exporters and China

Sharp global price declines

“Too much milk for the market, combined with strong milk solids growth, has contributed to a sharp decline in commodity prices,” Mr Harvey said.

“Butter has led the decline, down nine per cent since the beginning of October, and 24 per cent below its peak earlier this year. Whole milk powder (WMP) and cheese have also followed suit, each seven per cent down on the beginning of this quarter. Skim milk powder (SMP) prices have held up better though, declining a mere one per cent from already low prices felt earlier in Q3.”

Looking forward to 2026, the RaboResearch report said, a period of weaker commodity prices was likely in the face of ample milk supplies and exportable surpluses.

“Demand remains fragile and, in the absence of any supply shock to impede surplus milk, this raises the risk of prolonged weak pricing through mid-to-late 2026 as surplus milk enters the market,” Mr Harvey said. “However, supply growth is expected to slow to just 0.12 per cent next year, and weaker prices should eventually support a gradual recovery in demand, with commodity prices expected to return to historical averages by year-end 2026.”

Australia

In Australia, milk production has passed its peak for the current season, the report said.

“Milk production is down 2.3 per cent season to date (October 2025) on the previous year, led by declines in Victoria, the largest production state,” Mr Harvey said.

“This rate of decline has slowly started to moderate though, with October bringing much-needed rainfall in some dairying regions in southern Australia and with further rainfall in November.”

RaboResearch expects overall Australian dairy production to finish the current season (at the end of June 2026) down 1.2 per cent on the previous season.

The report said Australian dairy export volumes are under pressure from the reduction in milk supply. “Dairy exports volumes fell 2.6 per cent year-on-year in the September quarter,” Mr Harvey said.

“Milk and cheese exports remain robust, but there are large percentage falls in fat, whole milk powder and whey exports.”

There is positive news though when it comes to local feed markets, Mr Harvey said, with more grain crops being cut for hay, which has helped lower feed prices from recent record highs.

“Meanwhile, weak global grain prices and a large winter crop expected from the current Australian harvest means purchased grain is ample and prices are largely affordable for dairy farmers.”

On the retail side, Mr Harvey said, dairy price inflation ticked higher in Q3 2025. Milk prices rose 1.3 per cent year-on-year in the September quarter, while retail cheese prices increased 1.4 per cent year-on-year.

The report noted that “the high protein dairy boom is alive and well” in Australia, with recent market reports indicating double digit growth in the category leading to local supply chain shortages.

<ends>

RaboResearch Disclaimer: Please refer to Australian RaboResearch disclaimer here

Media contacts:

Denise Shaw Will Banks

Media Relations Media Relations

Rabobank Australia & New Zealand Rabobank Australia

Phone: 02 8115 2744 or 0439 603 525 Phone: 0418 216 103

Email: [email protected] Email: [email protected]

About us:

Rabobank Australia & New Zealand Group is a part of the international Rabobank Group, the world’s leading specialist in food and agribusiness banking. Rabobank has more than 125 years’ experience providing customised banking and finance solutions to businesses involved in all aspects of food and agribusiness. Rabobank is structured as a cooperative and operates in 38 countries, servicing the needs of more than nine million clients worldwide through a network of more than 1000 offices and branches. Rabobank Australia & New Zealand Group is one of Australasia’s leading agricultural lenders and a significant provider of business and corporate banking and financial services to the region’s food and agribusiness sector. The bank has 87 branches throughout Australia and New Zealand.